Alright folks, let's get real here. The ABA number meaning is more important than you might think, especially if you're dealing with banking transactions. But what exactly is this mysterious code? Let me break it down for ya. It's like the secret password that banks use to make sure your money goes where it's supposed to go. So, if you've ever wondered why those nine little digits matter so much, stick around because we're about to spill the tea.

Now, before we dive deep into the nitty-gritty, let's talk about why understanding ABA numbers is crucial. Whether you're setting up direct deposits, paying bills online, or transferring funds, having the right ABA routing number can save you from a world of headaches. Trust me, nobody wants to deal with a bounced check or a lost payment, right?

And here's the kicker – it’s not just about knowing what an ABA number is. It’s also about understanding how it works and how to use it properly. So, buckle up because we're about to take a deep dive into the world of ABA numbers, and by the end of this, you'll be a pro at navigating the banking system like a boss.

Read also:Bank Aba Meaning Unlocking The Secrets Behind This Financial Powerhouse

What Exactly is an ABA Number?

Let’s start with the basics. An ABA number, also known as the American Bankers Association routing number, is a nine-digit code that identifies your bank. Think of it as the bank's social security number. It helps ensure that your money gets routed to the right place when you're making transactions. Without it, your funds could end up in digital limbo, and nobody wants that.

These numbers were first introduced back in 1910, and they've been a staple in the banking world ever since. They're used for everything from processing checks to facilitating wire transfers. And while the concept might seem old-school, it's still as relevant today as it was a century ago.

Why is the ABA Number So Important?

So, why does the ABA number matter so much? Well, it's kind of like the GPS for your money. When you send funds from one account to another, the ABA number tells the banking system exactly where that money needs to go. Without it, your transaction would be like a letter without an address – it just wouldn't get delivered.

And let’s not forget about security. ABA numbers help prevent fraud by ensuring that only authorized transactions are processed. So, if someone tries to pull a fast one, the system can catch it before any real damage is done.

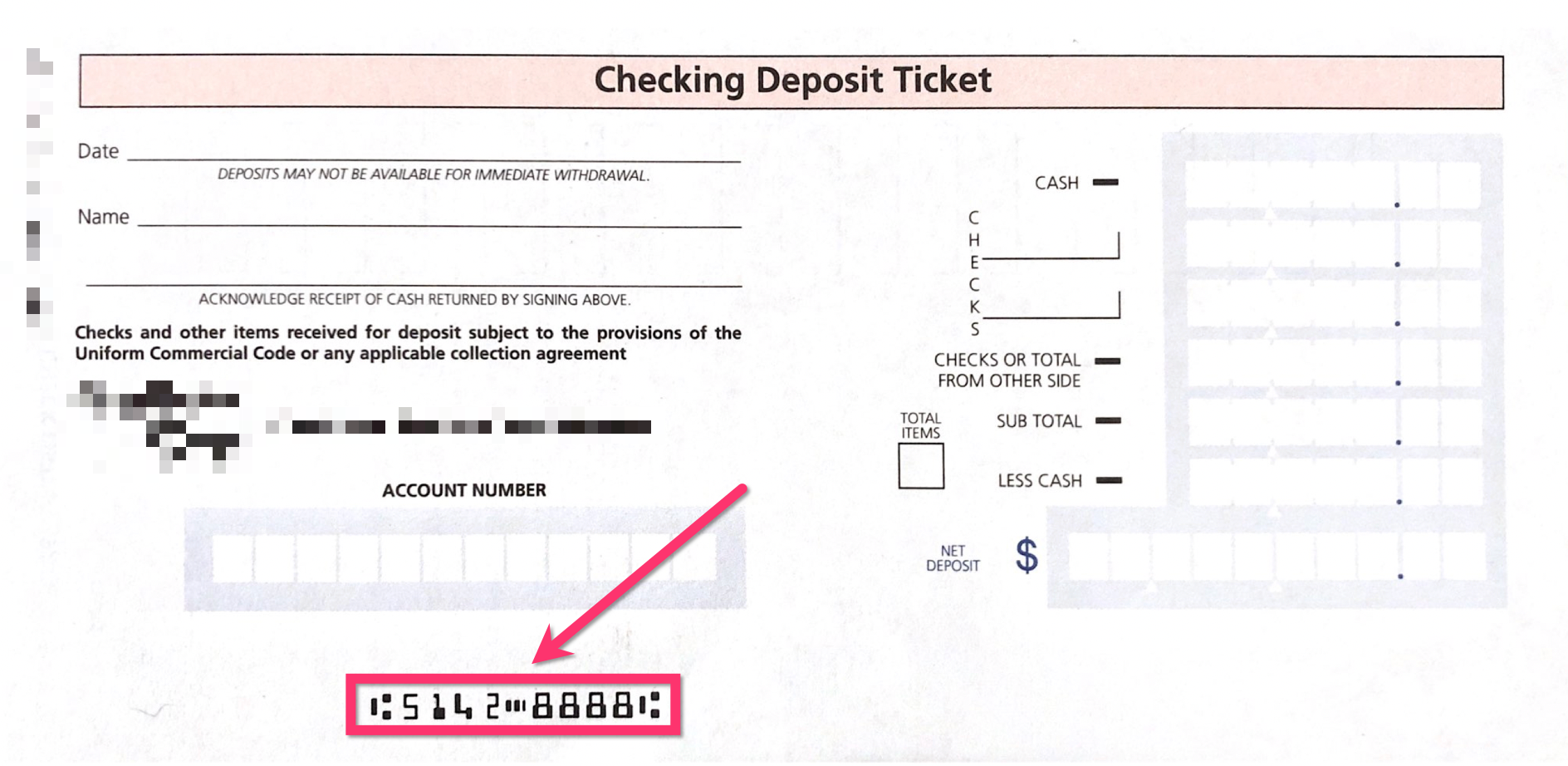

How to Find Your ABA Number

Finding your ABA number is easier than you might think. The most common place to locate it is on your checks. Look at the bottom left corner of the check – see those nine digits? That’s your ABA number. But what if you don’t have checks? No worries, my friend. You can also find it on your bank’s website or by giving them a quick call.

Here’s a pro tip: some banks actually have two different ABA numbers – one for wire transfers and another for ACH transactions. So, make sure you’re using the right one for the type of transaction you’re making. It might seem like a small detail, but it can make a big difference in how smoothly your transaction goes.

Read also:Is Hillary Farr Married The Inside Scoop On Her Love Life And Career

ABA Number vs. SWIFT Code: What's the Difference?

Now, here’s where things can get a little confusing. You might have heard of something called a SWIFT code. So, what’s the difference between an ABA number and a SWIFT code? Great question. While both are used to identify banks, they serve different purposes.

ABA numbers are used primarily for domestic transactions within the United States. On the other hand, SWIFT codes are used for international transactions. So, if you're sending money overseas, you'll need to use a SWIFT code instead of an ABA number. Makes sense, right?

How ABA Numbers Work in Transactions

Alright, let’s talk about the mechanics of how ABA numbers work in transactions. When you initiate a transfer, the ABA number is sent along with your account information to the receiving bank. The receiving bank then uses that ABA number to verify that the transaction is legitimate and to ensure that the funds are deposited into the correct account.

Here’s a quick breakdown of the process:

- Step 1: You initiate the transaction by providing your account information and the ABA number.

- Step 2: The sending bank verifies the information and sends it to the receiving bank.

- Step 3: The receiving bank uses the ABA number to confirm the transaction and deposit the funds into the correct account.

It’s a pretty straightforward process, but it’s important to double-check all the details to avoid any hiccups along the way.

Common Mistakes to Avoid with ABA Numbers

Now, let’s talk about some common mistakes people make when using ABA numbers. One of the biggest is using the wrong number for the type of transaction they’re making. Like I mentioned earlier, some banks have different ABA numbers for wire transfers and ACH transactions. Using the wrong one can delay your transaction or even cause it to fail altogether.

Another common mistake is entering the number incorrectly. Those nine digits might seem small, but they’re crucial. So, take your time and make sure you’ve got them right. And if you’re ever unsure, don’t hesitate to double-check with your bank.

The History Behind ABA Numbers

Let’s take a little trip back in time to explore the history of ABA numbers. As I mentioned earlier, they were first introduced in 1910 by the American Bankers Association. The goal was to create a standardized system for identifying banks and facilitating transactions. And boy, did it work.

Over the years, the system has evolved to keep up with changes in the banking industry. But the core concept remains the same – a unique identifier for each bank that helps ensure transactions are processed accurately and securely.

How Technology Has Impacted ABA Numbers

Technology has played a huge role in shaping the way ABA numbers are used today. Back in the day, these numbers were mainly used for processing checks. But with the rise of online banking and mobile apps, they’re now used for a wide range of transactions, from direct deposits to peer-to-peer payments.

And let’s not forget about security. With the increase in cyber threats, banks have had to implement more robust measures to protect ABA numbers and the transactions they facilitate. So, while the concept might be old, the technology behind it is constantly evolving to keep up with the times.

ABA Numbers and Online Banking

Nowadays, most people use online banking to manage their finances. And guess what? ABA numbers play a big role in that process. Whether you’re setting up direct deposits, paying bills online, or transferring funds between accounts, you’ll likely need to provide your ABA number at some point.

One of the coolest things about online banking is how easy it makes managing your ABA number. Most banks have systems in place that allow you to store your ABA number securely, so you don’t have to enter it every time you make a transaction. This not only saves time but also reduces the risk of errors.

Security Measures for ABA Numbers

Security is a top priority when it comes to ABA numbers. Banks use a variety of measures to protect these numbers and the transactions they facilitate. For example, many banks require multi-factor authentication when you access your account online. This adds an extra layer of security and helps prevent unauthorized access.

And let’s not forget about encryption. When you enter your ABA number online, it’s usually encrypted to protect it from prying eyes. So, even if someone were to intercept the information, they wouldn’t be able to read it without the encryption key.

ABA Numbers in the Modern Banking Landscape

As the banking landscape continues to evolve, so does the role of ABA numbers. With the rise of fintech companies and digital wallets, the way we think about banking is changing. But one thing remains constant – the importance of ABA numbers in facilitating transactions.

In fact, many of these new players in the banking world still rely on ABA numbers to process transactions. Whether you’re using Venmo, PayPal, or any other digital payment service, there’s a good chance that an ABA number is involved somewhere in the process.

The Future of ABA Numbers

So, what does the future hold for ABA numbers? While some might argue that they’re becoming outdated, I’d say they’re more relevant than ever. As long as banks continue to use them as a means of identification, they’ll remain a crucial part of the banking system.

That said, we might see some changes in how they’re used as technology continues to advance. For example, blockchain technology could eventually replace traditional ABA numbers in some scenarios. But until that happens, we’ll still be relying on those nine little digits to keep our money moving smoothly.

Conclusion

Alright folks, that’s the lowdown on ABA number meaning. From their humble beginnings in 1910 to their current role in the digital banking world, ABA numbers have proven to be an essential part of the financial system. Whether you’re a seasoned banking pro or just starting out, understanding how ABA numbers work can save you a lot of headaches down the road.

So, what’s the takeaway here? First, make sure you know your ABA number and how to use it properly. Second, be mindful of security when sharing this information online. And finally, don’t be afraid to reach out to your bank if you have any questions or concerns.

Now, it’s your turn. Got any burning questions about ABA numbers? Leave a comment below or share this article with your friends. And if you’re hungry for more financial knowledge, be sure to check out our other articles on the site. Until next time, stay smart and keep those funds flowing!

Table of Contents

- What Exactly is an ABA Number?

- Why is the ABA Number So Important?

- How to Find Your ABA Number

- ABA Number vs. SWIFT Code: What's the Difference?

- How ABA Numbers Work in Transactions

- Common Mistakes to Avoid with ABA Numbers

- The History Behind ABA Numbers

- How Technology Has Impacted ABA Numbers

- ABA Numbers and Online Banking

- Security Measures for ABA Numbers

- ABA Numbers in the Modern Banking Landscape

- The Future of ABA Numbers